Co.,Ltd.")

Co.,Ltd.")

CN

CN

EN

EN

Domestic DSP, unknown but breaking through soon

Although DSP (digital signal processor) belongs to the four mainstream processor series along with CPU, GPU and FPGA, although it has been widely used in mobile phones, home appliances, automobiles, high-speed rail, industrial control, drones and many other fields, compared with other processor series, it is significantly much more low-key, and even various controllers, SoCs, FPGAs are competing with it for living space.

Compared with the CPU, it is more specific and more efficient than FPGA computing. What is the development status of DSP in our country? What are the bottlenecks that break through? What is the future direction?

DSP is suitable for system low sampling rate, low data rate, multi-condition operation, and complex multi-algorithm tasks, and can quickly realize signal acquisition, transformation, filtering, valuation, enhancement, compression, identification, etc., to obtain the signal form that meets the needs. In the context of the digital era, DSP has become the basic device in communications, computers, consumer electronics and other fields.

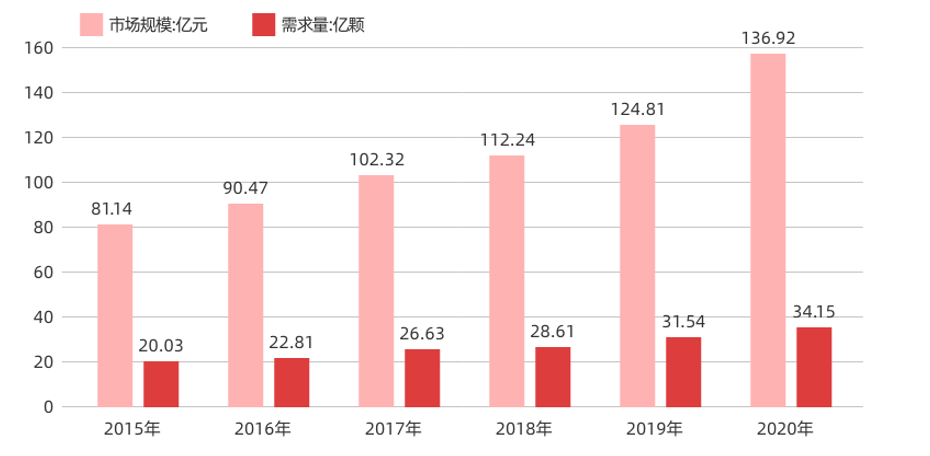

According to the data, in 2020, our country's DSP chip market size will reach 13.692 billion yuan, and the demand will reach 3.415 billion. The domestic DSP chip output will reach 91 million by 2020, although it has increased by about 3 times compared with 28 million in 2015, but it is still in huge contrast with the huge market size and demand, reflecting strong growth potential and urgent growth needs.

Statistics on the market size and demand of China's DSP chip industry from 2015 to 2020

Source: Zhiyan Consulting

2015-2020 DSP chip production trend chart in our country

Source: Zhiyan Consulting

Digital signal processors are not limited to the field of audio and video, they are widely used in communication and information systems, signal and information processing, automatic control, radar, military, aerospace, medical, household appliances and many other fields. From the perspective of consumption structure, the communication field is the largest application field of DSP chips, accounting for 56.1% in 2020, followed by consumer electronics-grade automatic control (13.10%), military and aerospace (6.01%) and instrumentation (24.79%).

our country's DSP chip consumption is much higher than the output, mainly because this field has been dominated by foreign manufacturers such as Texas Instruments (TI), Arc Devices (ADI), and NXP (NXP), which have accumulated many years of hardware research and development experience and a perfect software development environment, and the user ecology is relatively complete. The development of DSP in our country started late, and a high degree of localization has been formed in military radar and other fields, but it urgently needs to make a breakthrough in the civilian market.

DSP technology development has roughly gone through 4 stages:

The era of single-core and single-operation components

There is a dedicated hardware multiplier and an address generator with computing power inside the device, and the system mainly adopts Harvard structure;

Multi-compute component stage

With the deepening of DSP applications, the requirements for signal processing and computing power of the system increase rapidly, and improving the computing power of DSP devices has become the main goal, and increasing the number of internal computing components of the device is the most direct and effective means to improve the computing power.

Isomorphic multicore stage

Multi-core processors allow each processor core to complete different tasks, increasing the flexibility of processor applications.

Heterogeneous multinuclear stage

With the further improvement of process technology, it is possible to integrate different processor cores on a chip, for example: CPU focuses on general data processing, DSP focuses on real-time data calculation, and the combination of the two can greatly improve processing efficiency.

Several generations of product updates from TI and ADI, the world's leading DSP manufacturers, have almost experienced these developments. After several generations of product changes, DSP currently forms two main product forms: one is a single chip, and the other is integrated in the SoC in the form of IP or processing units. With the development of multi-core heterogeneous trends, single-chip, independent DSPs are increasingly turning to a single processing unit of SoCs.

This can also be verified from the business strategy of upstream IP licensors. CEVA, the world's No. 1 DSP IP licensor, has shifted from focusing on DSP programming to focusing on the entire ecosystem, building a larger platform for DSP applications. At present, CEVA has two main service methods, one is to license IP to IDM and indirectly serve OEM, and the other is to directly or indirectly serve OEM by providing development tools, technical support and software. Further expand the application market of DSP from the ecosystem and value supply chain.

The demand for high-speed and high-intensive data processing is constantly challenging the performance limits of DSPs. In the future, DSP technology will show five major development trends:

With the integration of DSP, more and more devices need to embed DSP functions, which can be implemented in the form of DSP cores or hardware DSP units.

Co.,Ltd.")